Employee stock option plans (ESOPs) have become popular amongst corporates, especially in the IT industry, to attract and retain talent. Different schemes are introduced by the employers; however, the complete benefit accrues to the employees when the lock-in conditions are met; or vesting period is completed by the employees.

Before you understand the taxation of ESOPs and RSUs, here are some key terms you must know:

- ESOP – or Employee Stock Option Plan allows an employee to own equity shares of the employer company over a certain period of time. The terms are agreed upon between the employer and employee.

- Grant Date –The date of agreement between the employer and employee to give an option to own shares (at a later date).

- Vesting Date – The date the employee is entitled to buy shares, after conditions agreed upon earlier are fulfilled. This date is also the agreed-on grant date.

- Vesting Period – The time period between the grant date and vesting date.

- Exercise Period – Once stocks have ‘vested’, the employee now has a right to buy (but not an obligation) the shares for a period of time. This period is called exercise period.

- Exercise Date – The date on which employee exercises the option.

- Exercise Price – The price at which employee exercises the option. This price is usually lower than the prevailing FMV (fair market value) of the stock. An employer and employee agree on ESOP terms on the grant date. Once the employee has fulfilled the conditions or the relevant time period has elapsed, these employee stock options are vested. At this time the employee can exercise them or put simply – buy them. The employee is allowed some time period during which this option to buy can be exercised. Once the employee decides to buy, these stock options are allotted to him at an exercise price which is usually lower than the FMV of the stock. Of course, the employee can choose not to exercise his option. In that case, no tax is payable.

Calculating Taxes

ESOPs are taxed at 2 instances –

- At the time of exercise – as a prerequisite – When the employee has exercised the option, basically agreed to buy; the difference between the FMV (on exercise date) and exercise price is taxed as perquisite. The employer deducts TDS on this perquisite. This amount is shown in the employee’s Form 16 and included as part of total income from salary in the tax return.

- Budget 2020 amendment – From the FY 2020-21, an employee receiving ESOPs from an eligible start-up need not pay tax in the year of exercising the option. The TDS on the ‘perquisite’ stands deferred to earlier of the following events:

- Expiry of five years from the year of allotment of ESOPs

- Date of sale of the ESOPs by the employee

- Date of termination of employment

- Budget 2020 amendment – From the FY 2020-21, an employee receiving ESOPs from an eligible start-up need not pay tax in the year of exercising the option. The TDS on the ‘perquisite’ stands deferred to earlier of the following events:

- At the time of sale by the employee – as a capital gain – The employee may choose to sell the shares once these are bought by him. If the employee sells these shares, another tax event happens. The difference between the sale price and FMV on the exercise date is taxed as capital gains. Exercise price ——-<Perquisite>——-FMV on exercise date——<capital gains>——sale price

| At the time of | Units | Date | Exercise Price | FMV of share* | Tax impact | Rate of tax | Tax to be paid | In income tax return |

|---|---|---|---|---|---|---|---|---|

| Grant | 100 | 1-Apr-12 | 100 | 120 | nil | nil | nil | |

| Vesting | 100 | 1-Apr-14 | 100 | 150 | nil | nil | nil | |

| Exercise | 100 | 1-Jul-14 | 100 | 170 | Taxable amount = FMV on Exercise date (1st July 2014) less Exercise Price | Income tax slab rate | Tax = 30% x 100 shares x (Rs 170 – Rs 100) = Rs 2100 and 3% cess on it | Under Income from Salary |

| Sale of shares if listed | 20 | 1-Oct-14 | 250 | Taxable amount = Sale Price on date of sale less FMV on exercise date | 15% on short term capital gains | Tax =15% x 20 shares x (Rs250 – Rs170)= 240 and 3% cess on it | Under Capital Gains (short term capital gains) | |

| Sale of shares if listed | 80 | 1-Sep-16 | 300 | nil, long term capital gains on listed shares is exempt from tax | long term capital gains are exempt | nil, long term capital gains on listed shares is exempt from tax | Exempt Income | |

| Sale of shares if unlisted | 20 | 1-Oct-14 | 250 | Taxable amount = Sale Price on date of sale less FMV on exercise date | Income tax slab rate | Tax =30% x 20 shares x (Rs250 – Rs170)= 480 and 3% cess on it | Under Capital Gains (short term capital gains) | |

| Sale of shares if unlisted | 80 | 1-Sep-16 | 300 | Taxable amount = Sale Price on date of sale less FMV on exercise date | 20% tax on long term capital gains after indexation of cost | Tax = 20% x 80 shares x (Rs 300-Rs 170*CII for 2016-17/CII for 2014-15) = 20% x 80 x (300 – 170*1125/1024) = Rs 1811 and 3% cess on it | Under Capital Gains (long term capital gains) |

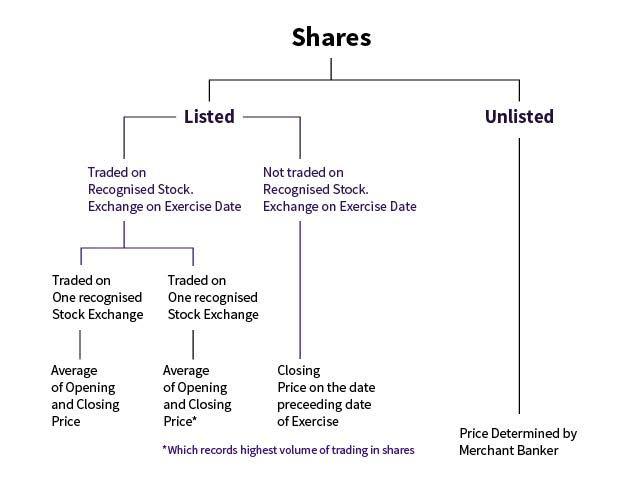

How to calculate FMV

Advance Tax on capital gains

Advance Tax rules require that your tax dues (estimated for the whole year) must be paid in advance. Advance tax is paid in instalments. While the employer deducts TDS when you exercise your options, you may have to deposit advance tax if you have earned capital gains. F

For FY 2021-22 for individuals instalments are due on 15th June, 15th September, 15th December and 15th March. By 15th March 100% of your taxes must be paid. See more details about advance tax here.

Non-payment or delayed payment of advance tax results in penal interest under section 234B and 234C. However, it may be hard to estimate tax on capital gains and deposit advance tax in the first few instalments if a sale took place later in the year.

Therefore when advance tax instalments are being paid, no penal interest is charged where instalment is short due to capital gains. Remaining instalment (after the sale of shares) of advance tax whenever due must include a tax on capital gains.

Other considerations involved

To properly calculate tax on the sale of ESOPs certain other aspects need to be considered as well.

Short term or long term gains

The rates at which your capital gains shall be taxed depends on the period of holding them. The period of holding is calculated from the exercise date up to the date of sale. Equity shares listed on a recognised stock exchange (where STT is paid on sale) are considered as long-term gains when held for more than one year. If sold within one year, they are considered as short-term gains. Currently, long-term gains on listed equity shares are taxed at 10% without indexation on LTCG above Rs 1 lakh, whereas short-term capital gains are taxed at 15%.

When you have incurred a loss

In case you have incurred a loss you are allowed to carry forward short term capital losses in your tax return and adjust & set them off against gains in future years.

Listed or unlisted shares

The Income Tax Act differentiates between tax treatment of listed and unlisted shares. The tax treatment for shares that are unlisted in India or listed out of India remains the same. That is, if you own shares of an American company, they will not be listed in India.

They may be considered unlisted for the purpose of taxes in India. The shares are short-term when held for less than 3 years and long-term when sold after 3 years. Starting FY 2016-17, UNLISTED equity shares shall be short term capital assets – when sold within 24 months of holding them and long term capital assets – when sold after 24 months of holding them [Applicable for sales made on or after 1st April 2016].

The period of holding begins from the exercise date up to the date of sale. In this case, short-term gains are taxed at income-tax slab rates and long-term gains are taxed at 20% after indexation of cost.

Residential status

Your income is taxable in India according to your residential status. If you are a resident, all your income from anywhere in the world are taxed in India. On the other hand, if you are a non-resident or resident but not ordinarily resident and have exercised your options or sold your shares, you may have to pay tax outside of India. In such a case, you may be able to take the benefit of Double Taxation Avoidance Agreement (DTAA). It makes sure your income is not taxed twice.

Disclosures

Several disclosures have been added in income tax return forms for foreign assets. If you own ESOPs or RSUs of a foreign company, you may have to disclose your foreign holdings under schedule FA of your income tax return. These disclosure requirements are applicable to a resident taxpayer.

When options are not exercised

On the vesting date the employee gains a right to exercise his option or buy the stocks. But there is no obligation, employee can choose to not exercise his option. In such a case there shall be no tax implication for the employee.